Before we dive in, don't miss our free webinar on June 27th, "How to Win in Cloud GTM with Key Strategies and Automations." Scroll below to learn more or check out the webinar page here.

Now, let’s explore why the marketplace model is the future of B2B e-commerce and what it means for your cloud GTM strategy.

_________________________________________

Marketplace Model: The Future of B2B E-commerce?

B2B e-commerce is undergoing a seismic shift, with the marketplace model emerging as a clear winner. BCG data reveals that marketplace growth is outpacing traditional e-commerce by 7X. But what's driving this explosive growth?

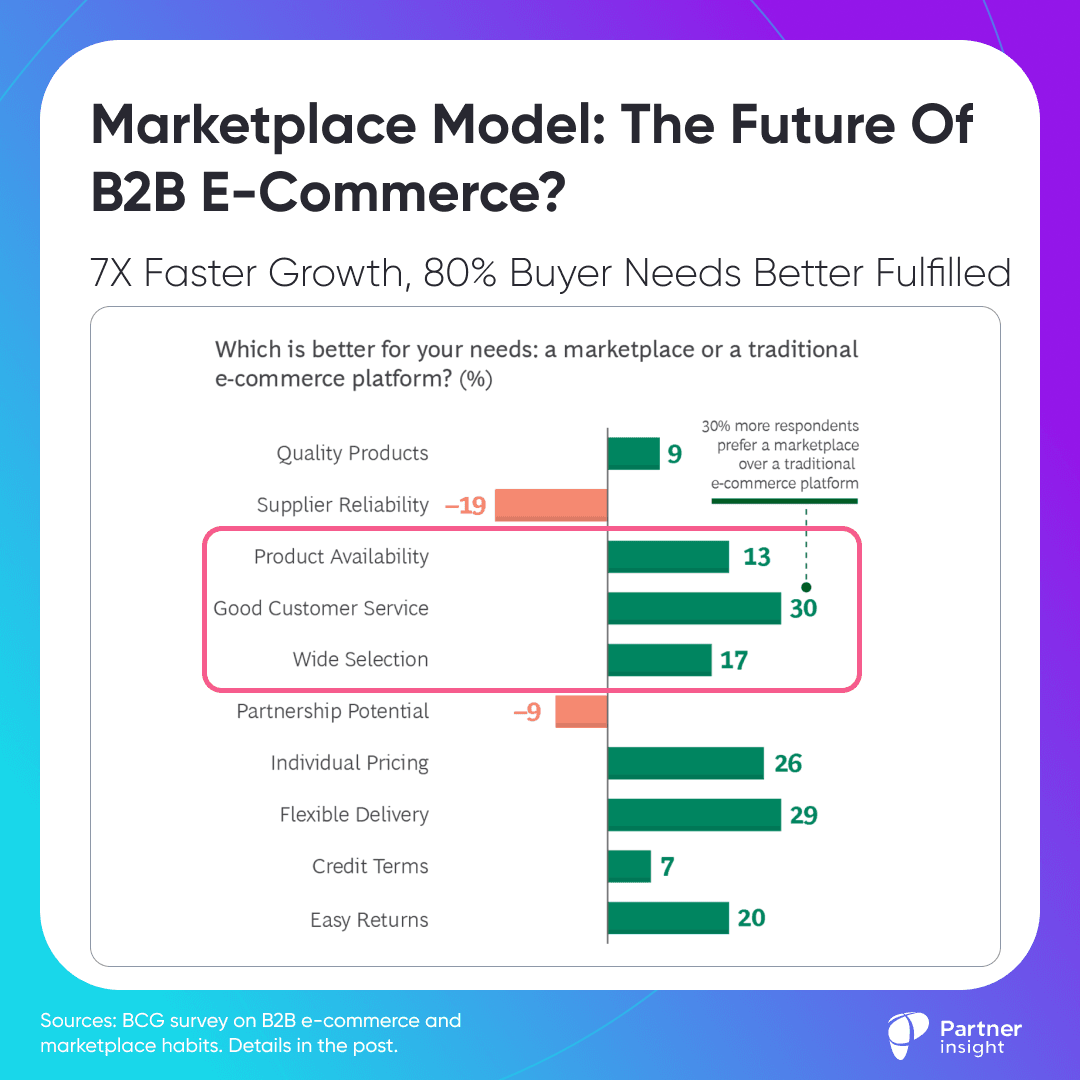

B2B buyers prefer the marketplace model, because 8 out of 10 of their most important needs are fulfilled better through marketplaces than traditional e-commerce sites (see the image). This drives much faster growth of marketplaces than traditional e-commerce, which is growing fast in itself.

This data comes from a newly published BCG survey on B2B e-commerce and marketplace habits. While it covers traditional B2B marketplaces, it's easy to see how these insights apply to hyperscaler marketplaces as well.

B2B E-commerce Expansion

B2B e-commerce continues to expand rapidly, with global sales hitting $23.4 trillion in 2023 and a growth rate of 16%. Sales in North America and Europe reached $4.8 trillion. The trend toward online sales shows no sign of slowing down, with over 50% of SMBs planning to increase their online procurement spending in the coming year.

The marketplace model is growing at a rate seven times faster than traditional e-commerce because it creates efficiencies for buyers, sellers, and marketplace operators.

Buyers Prefer Choice and Convenience

B2B buyers believe this model is superior, because marketplaces offer B2B buyers easier access to a wider range of quality products, better availability and visibility of inventory, good customer service, flexible delivery, and individual pricing.

BCG respondents highlight that "the marketplace offers time savings for buyers by allowing them to compare a wide range of products, prices, delivery times, and service quality all in one place."

Sellers Like Scale and Access

Why do sellers prefer marketplaces? Sellers participate in marketplaces to expand customer reach, increase geographic coverage, and reduce the need for a large salesforce along with associated selling costs.

Why Are B2B Companies Launching Marketplaces?

Better Customer Proposition

Marketplaces act as a one-stop shop with an expanded range, so customers don’t need to look anywhere else. The marketplace model makes it easy to expand assortment and meet more customer needs in a scalable manner.

Operational Simplicity. Companies can focus on core products while fulfilling broad customer needs.

Economic Benefits: Marketplaces provide additional revenue streams

Data insights into customer needs and behavior.

Marketplaces Rely on High-Quality Sellers

A marketplace is most successful when it becomes a buyer’s exclusive and trusted procurement option, meaning it has everything a buyer needs and enough choices to trade off between price, delivery speed, and other considerations. Key to achieving this is having multiple high-quality sellers.

As a result, continuous recruitment of sellers is critical. More sellers mean more buyer choice. In turn, buyers have a more positive experience, which grows traffic and GMV.

This doesn’t mean opening the flood gates to sellers; the top two needs of B2B buyers in procurement are access to quality products and seller reliability. Consequently, seller expansion must be pursued thoughtfully and strategically. To maximize impact, prioritize sellers based on product relevance and reliability, as the top 10% of sellers often generate more than 80% of third-party sales.

Marketplaces Change The Role of Sales Org

Launching a marketplace significantly changes a company's business and, notably, the role of the sales organization. It’s essential that the sales team fully understands and appreciates the benefits of this new platform so they can effectively promote it to customers. The primary advantage to communicate is that buyers can compare various types of parts, prices, delivery times, and service quality, saving them time and providing them with products that optimally meet their needs. Over time, this will also alter the nature of the sales team’s role within the business, helping buyers understand and expand the use of the platform versus selling products.

Finally, marketplaces require major tech investments from their operators as we already discussed before. They need a dynamic, cutting-edge tech architecture that integrates with existing systems and supports integration with third-party suppliers’ systems to display prices and inventory in real-time.

Whether you’re selling via cloud marketplaces or other B2B marketplaces, this can help you better understand the mindset of sellers, buyers, and marketplace operators. You can find the full BCG research here.

_________________________________________

AI Meets Cloud: Opportunities You Can't Ignore

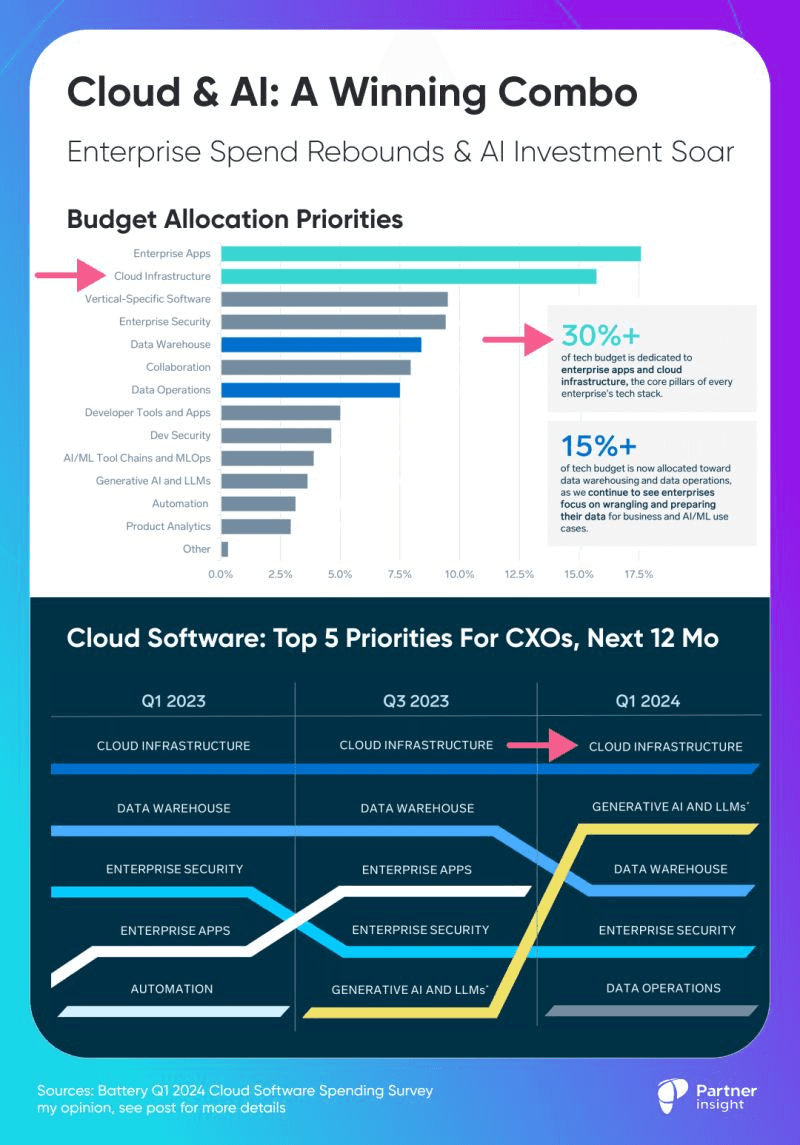

Cloud infrastructure remains the 💳 top spending priority for enterprises, with AI quickly climbing the ranks and challenging traditional enterprise applications.

This data from Battery Ventures Cloud Software Spending Survey Q1 2024 that included 100 enterprise CXOs representing nearly $36 billion in annual technology spend, tells a compelling story.

💰 Resilient and Growing Technology Spending

55% of enterprises plan to increase their technology budgets, with 8% planning a major >10% boost, which is twice as many as in Q3 2023.

Budget cuts are less of a concern, with only 22% planning to reduce their budgets, a 7% drop from Q3. For the 22% of CXOs planning to optimize their budgets, top priorities include vendor consolidation, optimizing SaaS licensing, reducing workforce, and migrating to the cloud.

🔀 AI Shifting Priorities

While more than half of enterprises plan to increase overall tech budgets, 79% of respondents (even larger proportion) are planning to increase their AI/ML budgets over the next 12 months.

Generative AI and LLMs have skyrocketed to the 2️⃣ priority for enterprise tech buyers, with enterprises now also refocusing on building the right data tooling to enable AI-powered applications.

To leverage AI, 90% of enterprises either use

✔️ Out-of-box solutions, e.g., GPT-4 API - 50%

✔️ Fine-tune a foundation model - 📍 40% (up from 30% just a quarter ago)

🔝 Enterprise Applications Still on Top, but AI Opens More Questions

Despite the momentum in AI and LLMs, the lion’s share of the budget is still allocated to existing priorities, with enterprise applications and cloud being on top with 📍 30% of combined spend.

While the budget spent on AI is much smaller compared to enterprise applications (below 10%), AI creates an opening for companies with an AI-native approach. Nearly half of enterprises (45%) are now interested in exploring new vendors for AI copilot capabilities.

⚡ Cloud Infrastructure’s Dominance

The AI platform shift in the tech market has reinforced the importance of cloud infrastructure spending for enterprises, significantly benefiting hyperscalers like AWS, Microsoft, and Google Cloud.

Their strategic positioning on the infrastructure layer, holding and helping to consolidate customer data (essential for AI), and enabling access to AI models, will help companies to unlock more AI use cases.

Hyperscaler partner ecosystems and cloud marketplaces, where enterprises can modernize and consolidate their enterprise application spend, also present a bullish case for them.

_________________________________________

Dynatrace's Secret Weapon: How Partners Drive 2/3 of Their $1.5B ARR

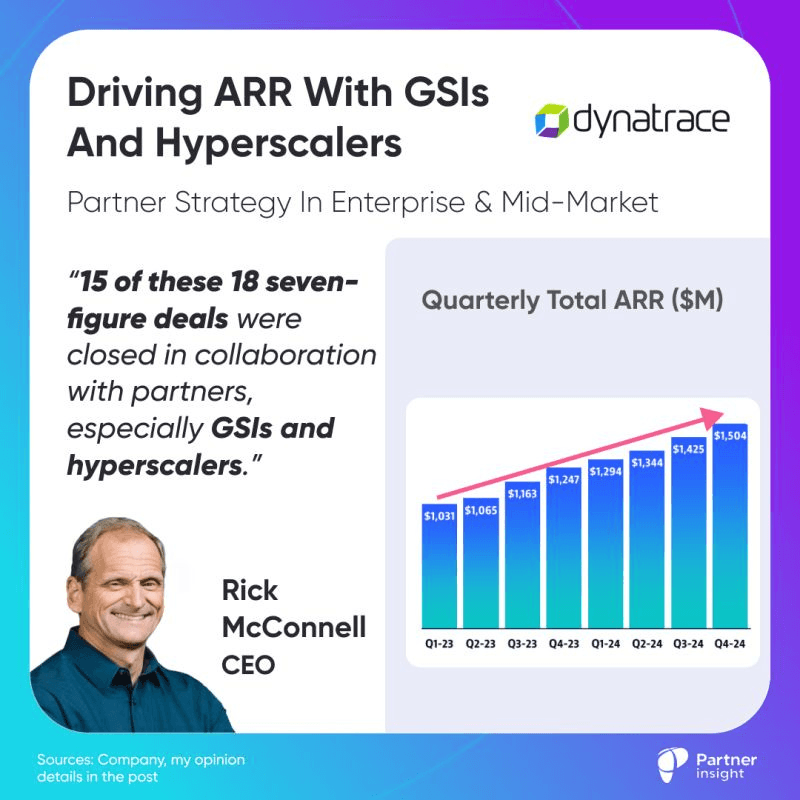

“Partners influence more than 2/3 of our ARR ''- stresses CEO of Dynatrace, with ARR surpassing $1.5Bn.

What's their strategy to 🎯 drive new revenue with partners, and why their “partner momentum is building”?

🏆 Record Wins in Collaboration with Partners

Dynatrace recently delivered a strong last quarter, finishing FY 2024 above the $1.5 Bn ARR milestone.

“We successfully closed numerous platform consolidation deals, contributing to a record 18 seven-figure ACV wins in the quarter” - highlighted Rick McConnell, its CEO.

Reflecting on the strong performance he adds that “15 of these 18 seven-figure deals were closed in collaboration with partners, especially GSIs and hyperscalers.”

📈 Partners and Hyperscalers Co-sell drive Net New ARR

Given this performance, it’s clear why the company made partners a top 3 pillar of their GTM strategy.

The CEO explained the opportunity:

“Partners, today, influence more than 2/3 of our ARR, but they account for only 30% of deal origination, highlighting the enormous whitespace of opportunity in this area.”

That’s why Dynatrace has added focus and simplicity to the core of their partner program.

“We are focusing our energy on our highest priority and most impactful partners. We are building a dedicated partner enablement engine to scale our priority partners.And we are simplifying our economic model with partner-neutral compensation and a co-sale approach with hyperscalers to remove friction and drive closer collaboration” - stressed the CEO.

💰 Driving Net New Deals with Partners

The focus on partners is for deal origination, explained Rick McConnell.

“The real thrust around our partner initiatives is to drive that 30% origination higher, which is precisely what we're doing with the GSIs and the hyperscalers.”

Dynatrace relies on partners to win not only in Enterprise, which is clearly working, but also in the Mid-Market.

📊 Mid-market Partner Strategy to Grow ARR & NRR

“Relative to the net new ARR... the strategy around mid-market is really partners. We talk about that a lot. We are definitely leaned in relative to GSIs and hyperscalers, and that is really how we would expect to attack the mid-market space.” - emphasized the CEO.

McConnell explained relative strengths of hyperscalers and GSIs across segments:

“We would expect GSIs to be headed up market, if anything. You look at the nine-digit TCV Accenture deal with a large global financial institution, that's the kind of thing that we're going to see out of GSIs.Hyperscaler engagements, we announced the partnership - GTM partnership with GCP in the past quarter as well. Those are the elements that will likely drive NRR in the mid-market.”

With hyperscalers driving such a significant portion of ARR for Dynatrace, how are you leveraging them in your GTM strategy?

Latest Insights & Analysis

We help our clients to define customer-centric strategies that stimulate innovation and create value